Unpacking MicroStrategy’s Bitcoin Strategy and Its Risks

Initially established as a business analytics software provider in 1989, MicroStrategy saw its shares plummet during the dot-com bubble. By 2020, the company had transformed, becoming the first publicly traded сompany to hold Bitcoin in its treasury.

Bitcoin crossed the $100,000 threshold for the first time following Donald Trump’s presidential election victory. Institutional adoption played a critical role in this historic milestone.

Prior to the launch of crypto ETFs, institutions often opted for “crypto stocks” – publicly traded securities that offered indirect exposure to Bitcoin and other digital currencies via traditional brokers.

Leading examples include Marathon Digital (MARA), a mining powerhouse; Coinbase (COIN), a major cryptocurrency exchange; and MicroStrategy (MSTR), a tech company with a bold Bitcoin strategy.

Let’s explore the strategic workings of MicroStrategy in this article.

Tracing the Roots of MicroStrategy

MicroStrategy Inc. (MSTR), founded in 1989 and based in Austin, initially gained prominence as a developer of enterprise analytics software. Its innovative solutions empowered businesses to process and draw insights from vast amounts of data.

The company’s stock, like many others in the tech sector, suffered during the dot-com collapse. However, MicroStrategy staged a comeback in 2020, becoming the first publicly traded corporation to focus on acquiring Bitcoin as a treasury asset.

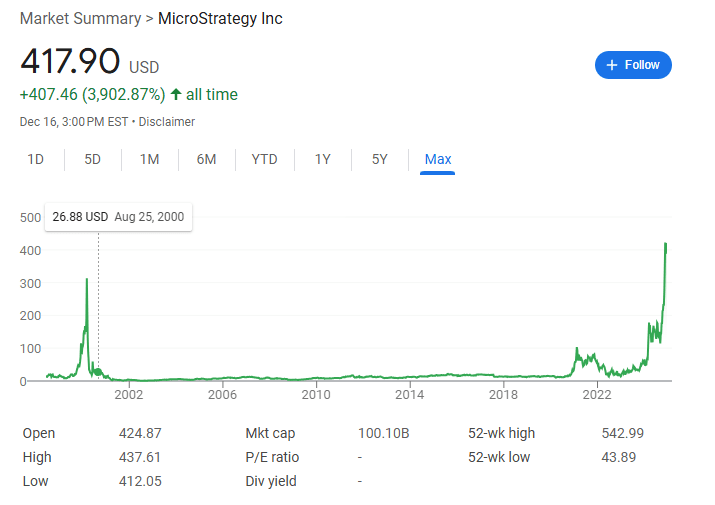

MicroStrategy (MSTR) Stock Trends. Source: google.com

While still providing business analytics services, the company now primarily focuses on Bitcoin investments as a defining part of its strategy.

MicroStrategy’s transformation took root in 2020 when Michael Saylor and the leadership team decided that relying on U.S. dollars for treasury reserves was suboptimal. Instead, they adopted Bitcoin as their primary reserve asset.

What started as a strategy to protect capital evolved into a pivotal link between equity markets and the crypto space. By issuing convertible notes and stock, the company accessed low-cost capital and reinvested it into Bitcoin acquisitions.

As of December 16, 2024, the company holds 439,000 BTC, worth $45.6 billion, with an average acquisition cost of $61,725 per Bitcoin.

How MicroStrategy’s Bitcoin Strategy Really Works

To fund its ambitious Bitcoin purchases, MicroStrategy relies on borrowed capital, primarily through the issuance of convertible notes.

These notes offer a blend of fixed income and equity potential, giving investors regular returns while allowing them to convert the notes into company shares under pre-established terms.

This financial strategy provides MicroStrategy with access to cost-effective capital, which it uses to acquire Bitcoin.

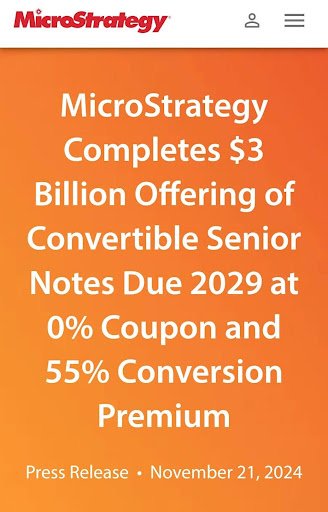

To expand its Bitcoin reserves, MicroStrategy offers convertible notes, either on fixed-income markets or directly to institutional investors. This method enables quick fundraising while keeping borrowing costs remarkably low.

The notes s appeal to investors by including an option to convert into MicroStrategy shares at a premium over the issuance price. Acting much like call options, they are particularly valuable during bullish Bitcoin trends when demand is on the rise.

MicroStrategy has crafted a strategy that amplifies itself. As Bitcoin prices climb, the premium on MSTR stock rises, making it possible to issue more debt or equity. The funds raised are then invested in additional Bitcoin, driving demand and pushing prices even higher, perpetuating a cycle that strengthens in bullish markets.

This mechanism enables MicroStrategy to leverage Bitcoin’s growth and investor appetite to expand its holdings significantly.

Latest fundraising round for Bitcoin purchases completed by MicroStrategy. Source: Official MicroStrategy Website.

MicroStrategy’s Strategy — Simplified for Everyone (Including Grandma)

Thanks for hanging in there! If the earlier explanation felt like a whirlwind, fear not. This section will walk you through MicroStrategy’s approach in the easiest way possible—grandma-approved simplicity included.

If you’re already an economic whiz, feel free to skip ahead to the next section!

Picture this: you own a business that’s breaking even. It holds $10 in its account, meaning its assets are worth $10.

You choose to invest that $10 in Bitcoin. If Bitcoin’s price doubles, your company’s total assets rise to $20. With your business entirely dependent on Bitcoin’s performance, the doubling of Bitcoin’s value directly doubles the company’s valuation.

But before committing your $10, you decide to borrow an additional $10 from a bank. Using your $10 in assets as collateral, the bank grants you the loan.

Although your company’s intrinsic value is still $10, taking out the $10 loan gives you $20 to invest. You channel the entire amount into Bitcoin, and when its price doubles, the total value of your holdings soars to $40.

Although your company’s intrinsic value is still $10, taking out the $10 loan gives you $20 to invest. You channel the entire amount into Bitcoin, and when its price doubles, the total value of your holdings soars to $40.

The process introduces leverage—borrowing to amplify returns on an investment. While this can magnify profits, it carries the risk of catastrophic losses if the asset’s price drops. MicroStrategy follows this leveraged approach to maximize its Bitcoin holdings.

An essential point is that leverage diminishes with Bitcoin’s price growth. Should Bitcoin double once more, your company’s value would rise to $80 (reflecting Bitcoin’s gain) less the $10 debt, totaling $70. In this case, the doubling of Bitcoin’s value doesn’t translate into a tripling of the company’s worth.

If no additional debt is incurred, the leverage effect wanes as Bitcoin’s price escalates. Over time, the leverage factor approaches 1, and the outstanding debt becomes nearly irrelevant to the company’s valuation.

MicroStrategy’s Strategy — Success or a Fragile Bubble?

Despite the undeniable success of MicroStrategy’s bold strategy, doubts persist. Could this strategy be skating on thin ice? Is the company at risk of riding a speculative bubble?

Currently, MicroStrategy’s market capitalization stands at $95 billion, compared to its Bitcoin holdings, valued at $45 billion. This results in a premium of 2.1x (210%) over its net asset value (NAV), effectively meaning the company’s market valuation exceeds its Bitcoin reserves by more than double.

The market has been buzzing with concerns over MicroStrategy’s high premium. The central issues revolve around its longevity and the potential repercussions if the premium drops significantly or becomes negative. Such a scenario could destabilize the company’s stock and disrupt its Bitcoin-fueled financial strategy.

Certain market players are exploiting the situation by shorting MSTR while acquiring Bitcoin as a hedge. Short interest in MSTR currently stands at roughly 11%, down from 16% reported in October 2024.

Evaluating the risk of MicroStrategy liquidating its Bitcoin reserves and the potential drop in the MSTR/BTC price or NAV premium requires considering another dimension—the condition of its aging software portfolio. This can shed light on the company’s ability to sustain its existing debt obligations.

The interplay between a significant debt burden and an elevated stock premium exposes the company to market volatility.

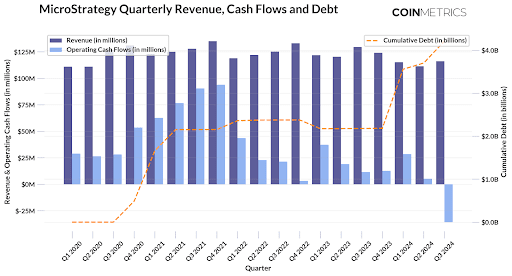

Q3 2024 MicroStrategy Earnings. Source: coinmetrics.com

The core software revenue of MicroStrategy has held steady since 2020, but its operating cash flows have experienced a gradual decline. Meanwhile, the company’s total debt has escalated significantly, reaching $7.2 billion.

This sharp debt increase stems from MicroStrategy's aggressive issuance of convertible notes to fund Bitcoin investments, particularly during market upswings. The data underscores the company’s dependence on Bitcoin price gains to sustain its financial footing.

Thanks to modest interest costs, these notess are likely supported by income from MicroStrategy’s core software business. If noteholders opt to convert their notes into shares when stock prices rise, the company could significantly reduce its debt without cash outflows.

Nevertheless, a decline in market conditions and a shrinking premium on MSTR shares could force MicroStrategy to reevaluate its options. This might mean selling off some of its Bitcoin assets or pursuing debt restructuring.

CryptoQuant — Only an Asteroid Could Sink MicroStrategy

MicroStrategy’s game plan relies on acquiring Bitcoin at increasingly higher prices by issuing debt to finance additional purchases. This often results in upward pressure on Bitcoin’s price, perpetuating a reflexive growth cycle.

Critics, however, remain skeptical. Chainlink’s Zach Reines has voiced his concerns, describing MicroStrategy’s debt-financed acquisitions as overly aggressive and stating that he feels "profoundly uncomfortable" with the company’s financial approach.

CryptoQuant CEO Ki-Young Ju stated that MicroStrategy’s Bitcoin trading would only be impacted by a major natural calamity.

In Ju’s view, the company’s bankruptcy is as unlikely as an asteroid hitting Earth. He emphasized that Bitcoin has stayed above the cost basis for long-term holders for the past 15 years, a figure now sitting at $30,000.

Ki-Young Ju explained that MSTR’s debt level, which sits at $7 billion, isn’t alarming when viewed alongside its Bitcoin holdings, valued at around $47 billion.

MicroStrategy — A Catalyst for Corporate Bitcoin Adoption

MicroStrategy’s daring approach showcases Bitcoin’s capacity to serve as a game-changing reserve asset for corporations. The company’s robust Bitcoin holdings have elevated its market presence and set it apart as a distinctive player in the crypto ecosystem.

Nonetheless, this strategy is not without its pitfalls. The volatility of Bitcoin and fluctuations in stock premiums present ongoing risks, requiring proactive management in an ever-shifting financial environment.

MicroStrategy’s model has the potential to encourage wider adoption of Bitcoin, with its influence possibly extending from private corporations to the realm of governmental policies. Such progress could further entrench Bitcoin as a trusted store of value and a critical reserve asset, underscoring its role in the global economy.

On December 23, 2024, MicroStrategy will officially become part of the Nasdaq 100, an index representing the largest 100 publicly traded companies in the U.S. This achievement is expected to strengthen investor sentiment toward both MSTR and BTC, likely driving increased interest and buying activity.

Stay tuned for an in-depth analysis on the implications of this Nasdaq 100 inclusion, coming soon to our website. Follow us on social media to stay in the loop.

What are the potential risks of MicroStrategy's Bitcoin strategy?

Recommended